Gold portfolio claims can sound exciting until you start asking what actually backs them up.

Garrett Goggin says Golden Portfolio IV is built around a rare gold setup tied to the petrodollar, undervalued miners, and a valuation gap he calls the “Golden Anomaly.”

Skeptical but interested, I dug into the biggest claims behind the service to see which ones hold up and which ones need caution in this Golden Portfolio IV claims review.

Why Portfolio Offers Need a Claims Review

Portfolio offers need a closer look because they ask you to buy into more than one stock idea: the thesis, the timing, the research process, and the person making the call.

That matters even more with gold. Gold offers emotional themes like inflation, war, debt, central bank money printing, dollar weakness, and loss of buying power.

That matters even more with gold. Gold offers emotional themes like inflation, war, debt, central bank money printing, dollar weakness, and loss of buying power.

Those concerns are real, but they can pressure you into acting before you understand the risk.

A strong offer should explain what is being recommended, why those assets may be mispriced, and what could go wrong.

GPIV is more interesting than a standard gold warning because Garrett ties his claims to NAV, market cap, free cash flow, ore grade, and production stage.

That framework is worth examining.

Claim #1: The Petrodollar System Is Under Pressure

Garrett’s biggest macro claim is that the petrodollar system is weakening, and I find this harder to dismiss than most newsletter macro arguments.

Garrett’s biggest macro claim is that the petrodollar system is weakening, and I find this harder to dismiss than most newsletter macro arguments.

Iran is now charging yuan-based tolls through the Strait of Hormuz.

That lane handles roughly one in five barrels of global oil. Garrett says more than 13.7 million barrels have been settled in yuan outside the US dollar system, with China buying more than 80% of Iran’s seaborne oil exports.

Saudi Arabia adds weight: the Kingdom let the old 1974 petrodollar arrangement lapse, signed a $7 billion currency swap with China, settled its first crude purchase in digital yuan, and joined mBridge in June 2024.

This claim is dramatic, but it is not random.

The real question is whether these shifts become large enough to weaken global dollar demand over time.

Claim #2: Gold Could Benefit From Dollar Weakness

Garrett’s next claim is that gold could benefit if the dollar loses part of its global oil advantage.

That logic is sound.

Gold often attracts attention when people worry about currency debasement, inflation, debt, and central bank policy.

Gold often attracts attention when people worry about currency debasement, inflation, debt, and central bank policy.

What I find useful is that GPIV does not stop at “buy gold.”

Garrett uses the dollar-pressure theme as a catalyst for a more specific search: gold-related assets that may offer more upside than bullion alone.

That is an important difference. A broad gold warning can get attention, but it does not give you a plan.

GPIV turns the macro claim into a search for select miners and royalty-style gold exposure. That is a more actionable structure.

Claim #3: Select Gold Miners May Beat Gold Itself

Garrett claims certain gold miners could outperform physical gold. I think this is one of the more believable claims, but only when applied to the right companies.

Gold can rise in price, but it does not create free cash flow.

A miner can benefit from higher gold prices, wider profit margins, stronger reserve values, and acquisition interest from larger mining companies.

That leverage is why miners can move much faster than bullion during a gold bull market. It is also why they can fall harder when gold pulls back.

Garrett says gold has risen more than 189% since September 2022, yet retail investors pulled $13 billion from gold ETFs in March 2026, even as gold sat near highs.

Meanwhile, the best gold companies saw cash flows double, triple, or quadruple since 2024. That mismatch supports the claim.

Meanwhile, the best gold companies saw cash flows double, triple, or quadruple since 2024. That mismatch supports the claim.

Claim #4: Most Gold Miners Are Not Worth Buying

This may be the most trust-building claim in the whole offer, and I appreciate that Garrett leads with it.Garrett says about 90% of gold miners make no profit and may never make money, regardless of where gold trades.

That sounds blunt, but it is a healthy warning in this sector.

Garrett backs this claim with 20 years of visiting mines and meeting management teams firsthand.

Porter Stansberry, founder of one of the largest independent financial research firms for individual investors, called him “the most knowledgeable gold investor in the world.”

That context matters when evaluating who is doing the screening.

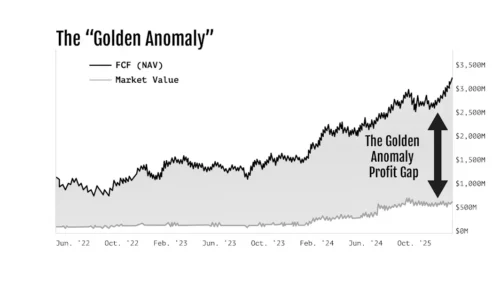

Claim #5: The “Golden Anomaly” Reveals Mispriced Miners

The “Golden Anomaly” is Garrett’s main valuation claim, and structurally, it is the strongest part of the offer.

He compares a miner’s Net Asset Value, the future free cash flow over the life of the mine, against its market cap.

He compares a miner’s Net Asset Value, the future free cash flow over the life of the mine, against its market cap.

Market cap shows what the stock market is currently paying for the company.

When NAV sits far above market cap, Garrett sees a possible mispricing. He calls that gap the “Anomaly Profit Variable.”

This is one of the strongest parts of GPIV because it gives the claim a measurable structure.

A miner is not attractive just because gold is rising. It needs a clear gap between price and value.

His Top Four picks trade at an average 64% discount to asset value, roughly 36 cents on the dollar.

One example: an $89 million market cap against a $1.5 billion NAV, pointing to a 94% discount and a 16.6X variable.

NAV discounts do not guarantee gains, but they give you something real to evaluate.

Claim #6: Past Winners Show the Upside Potential

Garrett uses past results to show what can happen when his thesis works.

Recent GPIV winners are listed at 115%, 515%, 1,307%, and 2,050%.

Earlier examples include Newmarket Gold at 2,200% and SilverCrest at 8,358% using the same Anomaly Profit Variable screen.

I would treat these as proof of potential, not a baseline expectation.

Promotions often highlight the best examples, and mining stocks can disappoint.

What makes the historical case credible is the methodology.

These were not random selections but companies identified through the same NAV discount screen Garrett applies today.

Claim #7: Royalty Companies Can Add a Different Gold Angle

Garrett includes a gold royalty pick as a bonus, and I think this is a smart structural addition.

A royalty company finances a mining project and collects royalties paid in gold for the life of the mine, with no mining operations or equipment costs.

Franco-Nevada’s Goldstrike royalty is the classic example: a $2 million investment became $1.2 billion.

That kind of result shows why royalty structures can be so powerful when the underlying mine performs.

Garrett’s current royalty pick is tied to Tether Gold, is up 139% this year, and has already returned over $17 million on a $200,000 stake.

This claim is compelling, but it still needs care. Royalty quality and counterparty strength still matter, but the structure gives the portfolio a different risk profile from the miners.

Claim #8: The Price Looks Low for the Research Value

The pricing claim is simple. GPIV currently costs $189 for one year and renews yearly unless canceled.

The pricing claim is simple. GPIV currently costs $189 for one year and renews yearly unless canceled.

Garrett holds a CFA designation, one of fewer than 200,000 worldwide, and a Certified Market Technician (CMT) credential.

His quarterly issues include detailed written reports on each of the Top Four picks, plus the bonus royalty pick, plus live model portfolio access and real-time fundamentals.

He frames this type of institutional-grade research as typically costing $2,000 or more.

I would not buy purely on that comparison, but $189 for four quarterly issues, live portfolio access, and a focused five-pick gold research service is a reasonable entry point.

How to Evaluate Any “Portfolio” Offer Like GPIV

A serious portfolio offer should answer a handful of practical questions before you subscribe.

Does it explain the catalyst? GPIV points to petrodollar pressure and a possible gold revaluation cycle with structural reasons from both the US and China sides.

Does it explain why the assets may be mispriced? GPIV uses NAV discounts, market cap gaps, free cash flow, ore grade, and production stage.

Does it acknowledge risk? Mining stocks are volatile, some projects fail, and gold can pull back. GPIV does not pretend otherwise.

Are the terms clear? Yes: $189 annually, yearly renewal, and a Golden Guarantee with a 25% test-drive fee.

Final Take: Are Golden Portfolio IV Claims Fair?

Final Take: Are Golden Portfolio IV Claims Fair?

Final Take: Are Golden Portfolio IV Claims Fair?

Final Take: Are Golden Portfolio IV Claims Fair?The claims behind Golden Portfolio IV are bold but not hollow.

The strongest claims are tied to Garrett Goggin’s valuation work.

The Golden Anomaly, NAV discounts, free cash flow focus, ore grade filters, and ore grade filters.

Newmarket Gold at 2,200%, SilverCrest at 8,358%, and recent picks up to 2,050% show what the framework can produce.

The petrodollar claim is dramatic, but it connects to a clear gold and mining thesis.

The extreme upside examples show a range of possible outcomes, not what every new pick will do.

For the names and valuation work, GPIV is the direct way to the research.

Tags:

Tags: