The property and casualty insurance industry, or simply P&C, is at the forefront of climate finance today. Severe hurricanes, typhoons, and natural calamities threaten residential and commercial structures. Those along and near the coastal areas are more exposed to these risks. As such, having insurance is necessary for households and businesses to ensure climate resilience.

The P&C insurance industry is becoming more of a staple in the US as climate change awareness increases. It has already become popular in many states, especially those along the Atlantic coastline.

One of these is Florida, a state that hurricanes have consistently visited. Yet, due to various challenges, many P&C insurance providers have become cautious about offering their products to the residents.

On a lighter note, the P&C insurance demand has considerably increased. While the state government remains the primary provider, private companies are essential. They bridge the gap between the amount the government can provide and how much the residents and businesses need.

In this article, we will cover the P&C insurance industry in Florida and give the top stock picks to help with your investment decisions.

Advantages of Investing in Florida-Based P&C Insurance Companies

Florida is one of the US’s most popular and important states, given its location and economic size. These are the advantages of investing in P&C insurance stocks in the state.

Economic growth

Florida ranks seventh among the fifty states in terms of the size of its economy. It ranks twelfth in business environment, fourteenth in employment, and seventh in growth. Overall, it ranks tenth.

Most importantly, it exuded economic resilience even during the pandemic’s peak. Its economic growth dropped but remained a positive value.

As of 3Q23, its real GDP growth rate reached 6%, prompting many analysts like JP Morgan Chase to bail on their recession call. Note that the third quarter of every year is when powerful and destructive hurricanes land in the US. Hurricane Ida in 2021 and Hurricane Ian in 2022 are some examples. In 3Q23, North Florida was severely damaged by Hurricane Idalia, a Category 4 hurricane.

Given all these, Florida’s healthy economy can support businesses despite the risks of natural calamities. Given the high median household income, the business sector can also thrive with the high purchasing power of the residents. All these contribute to high tax revenue, allowing the government to provide fiscal stimulus during an economic crisis.

High demand

Florida has a robust business sector, making it the eighth-best US state for businesses in 2023. Meanwhile, it is the third most populated state, with over 22 million residents. It’s no wonder Florida has many residential and commercial units built around it.

A home mortgage company sees a long list of applications, which may increase as inflation relaxes while the Fed maintains a rate hike pause.

Given all these, there is a high demand for P&C insurance to protect their properties in case of a natural calamity or man-made hazard. The robust economy and the high demand contribute to the strength of a P&C insurance business in the state. Customers have adequate capacity to sustain their payments.

In addition, the competition is not too tight, as several large insurance companies have left the state in the past four years. Hence, companies may capture new demand and expand their domestic market presence.

Risks of Investing in P&C Insurance Companies in Florida

Florida has rosy growth prospects, but some factors hold P&C insurance companies back from establishing here. In recent years, the state has faced problems, particularly insurance exodus, mainly due to these risks.

Location

The location of Florida is a double-edged sword for most P&C insurance companies. Since it has a high exposure to hurricanes, P&C insurance is a staple for households and businesses. The demand is high, allowing the companies to adjust rates depending on the season. However, it also means risks are higher during the third quarter of every year.

P&C insurance companies must indemnify their policyholders should a hurricane destroy their houses or offices. This leads to high insurance expenses and even cash burns. Note that a considerable portion of premiums paid by policyholders is invested in stocks, bonds, and others. An influx of claims will impact their liquidity.

Most importantly, four of the ten strongest hurricanes to have ever landed in the US directly hit Florida. Two of the costliest hurricanes in history were also in Florida. With that, even the P&C insurance companies are at risk of property destruction. As such, insurance companies can expect a huge plunge in net income during the hurricane season.

Roofing scams

Roofing scams are so rampant in Florida that they comprise over 70% of P&C insurance claim court hearings nationwide. This is how it happens. Roofing service providers connive with Florida residents to repair damaged roofs and have these paid for or replaced by P&C insurance providers. This malicious practice prompted the government to set specific standards before a policyholder could file for claims.

However, it did not make a massive change in the situation. Homeowners with a roof age of less than ten years have become the main complainants. And P&C insurance providers could hardly prove the connivance. Expenses from these roofing scams comprise a considerable portion of insurance expenses and drive the insurance exodus in the state, scaring insurance providers.

Pecking Orders

Among the several large P&C Insurance stocks, I trimmed them down to four to help with your investment decision. These are my P&C insurance top picks.

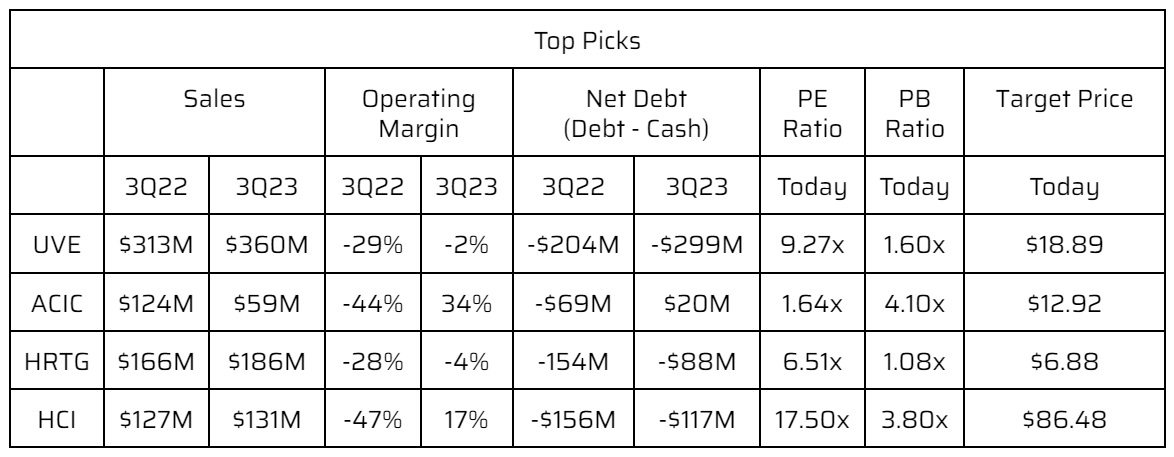

Universal Insurance Holdings, Inc. (UVE)

Universal Insurance Holdings, Inc., traded as UVE, is an integrated insurance holding company in the US. It develops and underwrites P&C insurance in personal and commercial lines. Also, it is one of Florida’s largest publicly traded P&C insurance companies.

Its over 30 years of existence have been through numerous powerful hurricanes, leading to severe destruction. Over the years, it had to repay hundreds of millions, which has consistently increased every third quarter.

Despite this, its long existence will testify to its durability and resilience. In fact, it had a year-over-year revenue growth of 15%, showing its increased demand and prudent portfolio diversification. Its operating margin was -2%, but we can attribute it to claims due to Hurricane Idalia. In addition, it was a massive improvement from -29% in the same quarter in 2022.

Note that the hurricane was much stronger than the hurricane last year. Most importantly, margins have always been reported as double-digit positive values in the other three quarters. It remains a highly viable company every year.

But what’s so great about this company is its high liquidity levels. Its Net Debt is -$299M, showing cash can cover all its debt in a single payment. Net Debt can also cover all claims even if it does not have to. As such, the company can sustain its business operations even if it does not generate net income.

Regarding its valuation, its PE Ratio of 9.27x and PB Ratio of 1.60x are lower than their five-year average. With that, the current stock price is cheap. If we use the enterprise value model, the target price will be $18.89, a 14% upside from its current price of $16.58. Hence, the stock is good for a buy position.

American Coastal Insurance Corporation (ACIC)

American Coastal Insurance Corporation (ACIC) was formerly United Insurance Holdings, Inc. (UIHC). It changed its name in line with its business restructuring and reorganization.

In recent years, it has endured the impact of the insurance exodus in Florida. It was also severely affected by Hurricane Ida in 2021, leading to a sharp plunge in its net income. To that end, it decided to forego its personal lines and instead focused on commercial lines.

This is a strategic move for the company. The P&C insurance market in Florida is not saturated, whether residential or commercial. Although most premiums are from personal lines, concentrating on commercial lines can benefit ACIC.

First, it can help the company avoid massive claims during the hurricane season. Second, it can avoid competition in the residential P&C insurance niche. The personal lines market has tighter competition than the commercial lines market. Plus, the government can be an indirect competitor.

This decision was a wise choice for ACIC. The operating revenue dropped by 52% in a year, but the operating margin improved substantially. The margin increased from -44% to 34%. This proves that most of its expenses come from its personal line segment.

Claims dropped from $117M (94% of sales) to $14M (24% of sales). With that, its move enhanced its efficiency, leading to a massive increase in viability.

Meanwhile, its liquidity remains decent despite the substantial increase in net debt. It has enough earnings to cover its net debt in a single payment. Even better, ACIC’s stock price is undervalued. It is traded at 1.6x its earnings. And if we use the enterprise value model, the target price will be $12.92, 11% higher than the current stock price. Hence, ACIC is also suitable for a buy position.

Heritage Insurance Holdings, Inc. (HRTG)

Heritage Insurance Holdings, Inc., or HRTG, became UVE’s closest competitor after ACIC disposed of its personal lines segment. It is also a large P&C insurance provider in Florida, although still much smaller than UVE. Yet, it is relatively newer among the three since it only started in 2012. Nonetheless, the company has thrived over the past decade.

Its revenue growth was also impressive at 12% despite the destruction brought upon by Hurricane Idalia. Thanks to the increased inflows of premiums. It was also driven by the tripling of its investment income, showing its wise allocation of its investments. Even better, its operating margin improved from -28% to -4%, proving its enhanced efficiency to offset the impact of hurricane-related claims.

It is also a highly liquid company, given its net debt of -$88 million. Its cash alone is enough to cover all its borrowings. The remaining portion can be used as reserves or reinvested. Even better, it is equivalent to nearly 20% of the total assets, making it a sustainable company.

Regarding its valuation, the stock is still reasonably priced. The current PE and PB Ratios are lower than the five-year average, but the difference is minimal. Also, the target price of $6.88 using the enterprise value model is 7% higher than the current stock price. Hence, there are still some upsides, but a bit limited, making it suitable for a hold position.

HCI Group, Inc. (HCI)

HCI Group, Inc. (HCI) is the most capitalized stock on the list. It has a market cap of $876M, nearly twice as much as UVE’s.

Like UVE and HRTG, it has capitalized on prudent M&As. It is relatively smaller than the two, but its continued expansion allowed it to go head-to-head with them. Its revenue growth in the third quarter of last year was low but decent at 3%. Yet, it had impeccable efficiency, which led to a massive increase in its operating margin to 17%. This makes HCI Group, Inc. the second most viable company on this list.

Additionally, it has sustainable core operations, given its net debt of -$117M. Its cash of $327M is 28% of the total assets, making it a very liquid company. It is also much higher than that of HRTG, making it the second most liquid company after UVE.

With regard to its traded price, the stock appears a bit overvalued. Its PE Ratio is much higher than the other three stocks and its five-year average. Also, the target price of the enterprise value model is $86.48, 4% lower than the current price. I will not recommend this as a sell, though, given its solid fundamentals. It’s just that the stock price is a bit high for a buy position right now. Hence, it is more sustainable for a hold position.

Conclusion

The P&C insurance market in Florida sees enticing growth prospects but faces some challenges. Yet, their evident resilience is an attribute investors should hold on to. Their fundamentals show they can withstand hurricanes while expanding amid economic recovery. Hence, investors must consider adding these stocks to their watchlist.

Tags:

Tags: