Artificial intelligence is taking the world by storm, but limitations due to the amount of energy data centers require are proving to be a major hurdle.

Joel Litman and Rob Spivey believe this problem is actually an opportunity for each of us as the one and only Elon Musk pursues a unique form of power generation.

In this Hidden Alpha review, I’ll break down the new “Dark Energy” angle, what the service includes, and whether there’s anything here actually worth paying attention to.

>> Get Hidden Alpha’s Dark Energy Picks <<

Hidden Alpha Explained: The Core Promise and Format

The forensic accounting methodology, Altimeter Database access, a live model portfolio, and a free year of The Timetable Investor make Hidden Alpha one of the more complete packages at this price point — especially for readers focused on the AI power grid story

The proprietary Altimeter Database lets subscribers independently grade any S&P 500 stock on demand, and the forensic accounting approach behind it is the same one that flagged Meta before a reported 1,400% run and AMD before a reported 7,100% run

The service is heavily concentrated in AI and energy themes right now, which limits sector diversification for readers who want broader market coverage from a single subscription

Hidden Alpha is a monthly newsletter and investment research service from Joel Litman and Rob Spivey. It’s published by Altimetry.

Joel has extensive experience as a forensic accountant, and he uses his skills to identify overlooked opportunities and market trends that could be on the path to breakout growth.

Subscribers receive these through the platform’s robust feature set, starting with its namesake newsletter.

How Hidden Alpha Works

Each month, members receive a new recommendation backed by clear analysis, plus access to tools that help them understand the bigger picture.

The service also tracks an active model portfolio you can check at any time and provides timely alerts when market conditions shift.

What I like is that it’s not just about stock tips but about uncovering opportunities before they ever reach the mainstream news.

>> Sign up NOW and SAVE 84% <<

Is Hidden Alpha Legit?

I’ve had the privilege of using Hidden Alpha for quite some time, and there’s nothing unscrupulous here.

The platform consists of a team of more than 100 financial analysts, accountants, and the like who specialize in locating these off-the-beaten-path opportunities.

While I won’t list them all here, some of the service’s biggest wins include Meta, Novawax, and AMD before they each enjoyed quadruple-digit gains.

Perhaps even more important are the big losses they’ve steered readers away from in 2008 and 2020.

The pièce de résistance, though, is the proprietary Altimeter system that filters promising picks in a way I’ve yet to see another service do.

Who Runs It, and What We Could Confirm

Let’s look a bit more closely at our gurus now:

Joel Litman

Joel Litman is the co-founder of Altimetry and serves as the Chief Investment Strategist of Hidden Alpha.

He is a Certified Public Accountant with a BS in Accounting from DePaul University and an MBA from Northwestern’s Kellogg School of Management.

In addition to his work with Hidden Alpha, Joel serves as the President and CEO of Valens Research. And he also sits on the board of directors at COL Financial Group, an Asian brokerage firm.

Joel’s also a member of the Association of Certified Fraud Examiners, a professional trade group focusing on forensic accounting.

Over the years, Litman has consulted for global financial institutions, hedge funds, and even U.S. government agencies like the Pentagon and the FBI.

Over the course of his career, he has had stints at Credit Suisse, Diamond Tech Partners, Deloitte, American Express, and other prestigious institutions, which tells me the dude really knows his stuff.

>> Get Joel’s current investment recommendations now! <<

Is Joel Litman Legit?

Joel Litman is as legit as they come.

His professional credentials are remarkable, and many prominent outlets have solicited him for his forensic accounting expertise.

Barron’s has quoted his work in the past, and he’s made appearances on CNBC. Forbes even interviewed him.

His research has been published in multiple outlets, and he has co-authored books on accounting and valuation practices.

The guru has also taught courses at Harvard Business School and the Wharton School.

He has also worked as a Professor at Hult International Business School, which was named a top-ranked international MBA program by Financial Times and The Economist.

Few research services can claim to have such a prominent expert on their roster.

What is Rob Spivey’s Role?

Rob Spivey enters the picture as Alimetry’s Director of Research. His background as a chartered financial analyst really shines through here.

During his career, Spivey has held prominent positions at The Abernathy Group, Legacy Capital Management, and Credit Suisse, all while earning accolades as a CFA Charterholder and member of the CFA Institute.

His knowledge of how market trends unfold allows him to leverage both the buy-side and sell-side of finance to bringh is audience the chance for gains.

An avid podcaster, Spivey has also presented his wisdom at higher learning institutions around the country.

Is Rob Spivey Legit?

Yes. Spivey has built his career by producing research used by some of the biggest asset managers globally.

His team’s work has been trusted by professionals from firms like Fidelity and Vanguard, and he has contributed to analyses that shaped investment decisions worth billions.

Sought after for his skills, Spivey has appeared on CNBC and been quoted in Barron’s, Bloomberg, Forbes, and a slew of other publications.

He’s even presented at prestigious schools such as DePaul University and the HULT International Business School.

With a CFA designation, Wall Street experience, and a track record of market calls, Spivey has proven himself a credible voice in financial research.

>> Claim Joel Litman’s Latest Research <<

What “Alpha” Means Here (and What It Usually Doesn’t)

Alpha is a term that describes the margin of difference between an investment’s performance and that of the overall market.

This metric basically quantifies how much a particular investment is outperforming the market as a whole. Typically, achieving alpha returns is the primary objective when investing.

Hidden Alpha gets its name from Joel and Rob’s ability to spot alpha opportunities that the market is overlooking using sophisticated forensic accounting analysis.

>> Join now for 84% off TODAY <<

What’s Inside Joel Litman’s “Dark Energy” Presentation?

Many world powers believe the leader of the AI revolution will become the world’s next superpower.

In our case, there’s a huge desire to stay on top of the totem pole, but we must first navigate the power bottleneck that’s keeping AI expansion to a minimum.

Joel and Rob believe the answer lies with a new project created by Elon Musk, who’s actively leading the charge on something they call “Dark Energy”.

I’d never heard about it before this point, but the gurus make it clear that this isn’t some sci-fi innovation.

Dark energy is already here, and it’s because you’ve never heard of it that makes it such an interesting investment opportunity right now.

Taking the Lid Off Dark Energy

No source of energy is perfect, and that poses a problem for data centers that need to run 24/7 without interruption.

Solar requires sunlight, the wind must blow for those massive turbines to rotate, and nuclear’s large footprint isn’t ideal.

Dark energy solves these problems in one fell swoop through a physics principle called electromagnetic induction.

I’m not here to give you a science lesson, but this tech first came to be nearly 200 years ago, so it’s nothing now.

The executive process is where the genius lies, generating power from incredibly fast-spinning blades.

It works in just about any environment and looks smaller than a semi trailer.

The Real Opportunity Sits With the Suppliers

If you’re hearing all this and thinking “there’s no way”, you’re not alone.

I want to remind you though that people thought the same thing about the light bulb, telephone, and even the internet.

The folks investing in those initiatives back in the day before they were on everyone’s radar were set to take the largest profits, not those waiting until everyone else was jumping in.

What I found most interesting though is that Joel and Rob call out the periphery companies that benefited the most from emerging tech.

Light bulbs needed glass to house them, and the internet is nothing without fiber optic cables to connect everything together.

As AI grows and embraces “Dark Energy”, the setup points toward a small group of suppliers that Big Tech will likely lean on.

How Readers Can Position Before the Story Gets Crowded

The takeaway is simple: AI’s next bottleneck likely won’t be software, chips, or cloud demand. It’ll be electricity.

Joel and Rob really like the setup, but they’re saying to ignore the energy itself and focus on the suppliers making it all happen.

Not every player will become a winner, which is why the research here is so on point.

By signing up for Hidden Alpha, you can get the scoop on which companies they believe are set to generate big profits and the ways you can get involved.

To that end, I want to unpack what comes with the service so you can see how everything comes together.

>> Unlock Hidden Alpha Before Headlines Hit <<

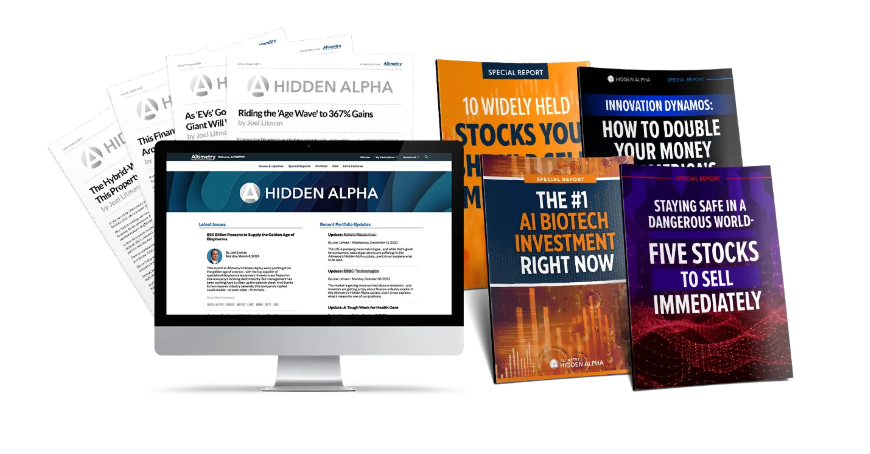

Hidden Alpha Review: What You Receive as a Subscriber

Here’s everything you get with a Hidden Alpha membership:

12 Months of Hidden Alpha

Every month, you’ll receive a new issue of Hidden Alpha with Joel Litman and Altimetry’s latest market research and best investment recommendation.

Like the current “Dark Energy” example, these opportunities capitalize on current and emerging trends with plenty of upside potential.

This research ties to the same team that recommended Meta to institutional clients in 2012 before it rose as much as 1,400%, and AMD in 2015 before it climbed as high as 7,100%.

Joel shares his findings using clear verbiage that’s easy to follow, and you’ll see names, ticker symbols, and the details you need to invest.

If Meta and AMD are any indication, getting in at this early juncture could make all the difference.

24/7 Access to Hidden Alpha’s Model Portfolio

The model portfolio gives members a central place to track Joel Litman and his team’s current buy and sell recommendations throughout the year.

The portfolio helps solve that by showing what the team still likes, what they have moved on from, and how their active ideas fit together.

All active positions show up here, so you’re not walking in the door empty-handed.

You can see how each one fares and invest in them as you see fit.

A fully invested Hidden Alpha portfolio would have returned 120% since inception. I would still review each position carefully, but having a live portfolio makes the service much easier to follow.

Special Updates

The special updates are perfect for keeping you in the know until the next monthly issue when something important changes.

Joel and his team email subscribers throughout the month when they believe it’s time to take action.

That can include locking in potential gains, adding to a position, closing one out, or reviewing new developments around an active recommendation.

I love receiving these because it means I don’t have to sit in front of a computer and watch for updates on my own.

It also takes away at least some of the emotional impact of investing and getting the timing down right.

>> See Joel Litman’s Top AI Picks <<

Friendly Customer Support

Hidden Alpha also includes access to Altimetry’s Customer Care team, based out of the Baltimore area.

Hidden Alpha also includes access to Altimetry’s Customer Care team, based out of the Baltimore area.

You can reach out Monday through Friday from 9 a.m. to 5 p.m. Eastern to get your questions about the service answered in a timely manner.

The support team covers everything from logging in, finding a report, canceling before renewal, and understanding where to access the archive.

Keep in mind you won’t get personalized financial advice here, but that shouldn’t be a surprise.

Joel’s Private Briefing From a Conference Attended by Google, Amazon, and Meta

This bonus video gives members extra behind-the-scenes footage from a conference that you won’t find anywhere else.

This bonus video gives members extra behind-the-scenes footage from a conference that you won’t find anywhere else.

In it, Joel shares details from an exclusive gathering of AI and energy executives, including key decision makers from Google, Amazon, and Meta.

That fits the new power grid theme well because these companies are directly tied to the data center energy race.

The real value here is context. Instead of only hearing that AI needs more power, subscribers get Joel’s closer look at what major tech and energy players are discussing behind the scenes as they search for reliable electricity.

Exclusive “War Room” Interview: The War in Iran and Your Investment Portfolio

The “War Room” interview adds a geopolitical layer to your membership.

The “War Room” interview adds a geopolitical layer to your membership.

In the past, Joel has personally consulted for the Pentagon, the FBI, and the Department of Defense, helping those agencies better understand financial markets.

In this bonus video, he sits down with a former high-level U.S. military commander to discuss the Middle East, China, and where the impact of war plays out.

We’ve already seen how global conflicts can affect oil, power, defense spending, supply chains, and market sentiment.

Learning how to get ahead of all that could be a huge win for your portfolio.

>> Access Hidden Alpha’s Power Grid Report <<

One Free Year of The Timetable Investor

This bundle also comes with one free year of The Timetable Investor, valued at $199.

It’s a second Altimetry research service led by Rob Spivey, the firm’s director of research.

While Hidden Alpha focuses on individual stock recommendations, The Timetable Investor looks beyond surface-level investments.

Each issue gives readers a straightforward projection of where the market could head next and how they recommend to position yourself.

I think of it as a supplemental tool to the other research here, giving you broader exposure to themes that could affect your positions.

The Altimeter Database

The Altimeter Database gives members subscriber-only access to Altimetry’s forensic stock-grading system that blows me away every time I use it.

You simply type in any S&P 500 ticker and can quickly see whether Altimetry views it as a good opportunity or a stock to avoid.

You’re in complete control over the stocks you search up, and even the reasoning behind them.

I often check on stocks I’m interested in buying, but it’s great for verifying what I have in my portfolio is still worthwhile.

For anyone who wants a second opinion before making moves, this database adds real day-to-day value.

>> Claim Joel’s Dark Energy Research <<

Digital Archive

The digital archive gives members access to past Hidden Alpha issues going back years.

It’s chock full of just about every investing topic you can think of, and several of the reports still have application today.

This helps newcomers catch up on older recommendations, past market calls, and the way Joel’s team explains different setups.

Not only can you use it as a learning library, it also helps unpack how Hidden Alpha handles risk and locates opportunities.

>> Access Joel’s latest reports and more HERE <<

Hidden Alpha Bonus Reports

The bonus reports are the most important part of the current Hidden Alpha deal if you are joining for the “Dark Energy” and power grid angle.

Featured Report: Dark Energy: Stocks That Could Soar as AI Goes Off the Grid

This is the centerpiece of the current Hidden Alpha research bundle, and it is the first report I’d recommend reading after joining.

This is the centerpiece of the current Hidden Alpha research bundle, and it is the first report I’d recommend reading after joining.

It contains the exact names and tickers of the supplier stocks Joel Litman believes sit at the center of the “Dark Energy” boom.

These are not the obvious AI names everyone already follows. The focus is on companies that could supply the critical infrastructure Big Tech needs as data centers demand more power.

Elon Musk, Sam Altman, and other major AI players may be early movers in this energy race, but they still need equipment, systems, and specialized infrastructure from outside companies.

Joel’s view is that some of these lesser-known suppliers could benefit as the $15 trillion AI industry tries to move beyond the limits of the traditional grid.

>> Follow Hidden Alpha’s AI Power Strategy <<

Bonus Report #1: Dark Energy, Phase 2: How to Profit as America Goes Nuclear

Dark Energy, Phase 2 expands the power grid story into small modular reactors, or SMRs.

Dark Energy, Phase 2 expands the power grid story into small modular reactors, or SMRs.

The idea is that “Dark Energy” turbines may help solve the near-term power shortage, but nuclear power could become the next major layer of AI infrastructure.

Traditional nuclear plants are too slow and too expensive for the current data center race, while SMRs are built around a smaller, more flexible model.

I appreciate the larger focus here that points to companies set to benefit from nuclear revival.

You’ll get all the details inside, down to the ticker symbols and how everything fits together.

Bonus Report #2: The Game Changers: Unbeatable-Advantage Stocks to Buy Today

The Game Changers takes the research beyond the power grid and back into AI’s next growth phase.

The Game Changers takes the research beyond the power grid and back into AI’s next growth phase.

The idea is that AI has crossed into a more powerful stage, where models are not just answering questions but improving, building, and automating at a faster pace.

If that shift continues, certain businesses could gain a lasting edge.

I think of this as the long-term growth side to “Dark Energy”, as these companies hold “unbeatable advantages” – things they do better than anyone else – that can take AI to a new level.

>> Get Joel Litman’s Supplier Stock Picks <<

Bonus Report #3: 10 Widely Held Stocks to Sell Immediately

Not every AI or energy stock will advance as trends shift. Some will get left in the dust as “Dark Energy” rolls out nationwide.

Not every AI or energy stock will advance as trends shift. Some will get left in the dust as “Dark Energy” rolls out nationwide.

Companies tied to outdated infrastructure, weak financials, poor energy positioning, or higher operating costs could struggle if the AI power buildout changes where capital flows.

The report names 10 stocks Joel believes could face serious pressure from this shift.

Some of these names may surprise you, but Joel’s explanations here make a lot of sense.

Warning lists like this are a key part of the Hidden Alpha approach, and this one gives you a chance to review what they already own before adding new ideas.

>> Sign up for latest Hidden Alpha Research under Joel’s guarantee <<

Hidden Alpha Pricing, Billing Terms, Renewals, and Upsells

First Year

$79

Regular

$499

Renewal

$199/year

after the first year

after the first year

The standard list price for a year of Hidden Alpha is $499, but right now, there is a steep discount available that makes it far more accessible.

New members can join for just $79 for the first year, an 84% savings compared to the regular cost. In the end, you’re paying just $1.50 per week.

This entry price includes every part of the service: the monthly newsletter, real‑time alerts, access to the model portfolio, and all of the bonus reports.

On top of that, you get that full year of the Timetable Investor and unlimited use of the Altimeter database that normally have huge price tags.

Once the first year is complete, you can re-up your service for $199, which still represents a substantial value given the breadth of resources provided.

>> Try Hidden Alpha Risk-Free Today <<

Claims and Track Record: How to Assess Them Responsibly

Joel Litman and Rob Spivey have a knack for pointing to major growth opportunities early, including Meta before its as high as 1,400% rise and AMD before its reported 7,100% run.

The current Hidden Alpha portfolio also has a stated return of 120% since inception for someone who followed the recommendations fully.

That gives the service a stronger performance story than many research letters in this price range, though I would still avoid treating any past result as typical.

What I also like is that Joel’s team has built part of its reputation on warning readers away from weak stocks.

Their past warning lists saw 17 stocks that later fell 90% or more, and Joel has also highlighted major risks before past market selloffs.

>> Access Joel Litman’s Power Grid Picks <<

Common Risks and Downsides (And How to Spot Them Early)

Investments always carry a sense of risk, no matter where the recommendations come from or how solid they seem.

Even on a research service like this with a solid track record, it’s important to know that there is a chance you may lose money, so keep expectations grounded in reality.

Never invest more than you can afford to lose, and always do your due diligence before making any type of investment.

As far as downsides go, Hidden Alpha currently feels AI heavy, so there’s not necessarily the diversity you’ll need to build a complete portfolio.

I personally supplement this with my own research, but not everyone has that kind of time.

Fit Test: Who Should Avoid Hidden Alpha

Monthly picks as seen in the format here are not a good fit for day trading.

Most newsletters of its ilk are not particularly suited for this type of trading, so I wouldn’t count it as a point against Hidden Alpha.

This hopefully won’t be a surprise, but the platform won’t download picks into your portfolio for you.

It does require effort to research recommendations given here on your own so you don’t end up somewhere you don’t want to be.

>> Join Hidden Alpha Before It Spreads <<

Pros and Cons of Hidden Alpha

I reviewed the updated “Dark Energy/Power Grid” version of Hidden Alpha, and these are the strongest pros and mild cons that stood out.

Pros

- One year of Hidden Alpha newsletter

- Focuses on AI power demand

- Covers “Dark Energy” supplier stocks

- Model portfolio and frequent updates

- Full digital archive access

- Multiple high-value bonus reports

- Free Altimeter Database access

- Includes Rob Spivey’s market service

- 84% discount on the first year

- 30-day money-back guarantee

Cons

- No community forums

- Focused heavily on energy and AI

- Discount applies to the first year only

Refunds, Cancellations, and Support Expectations

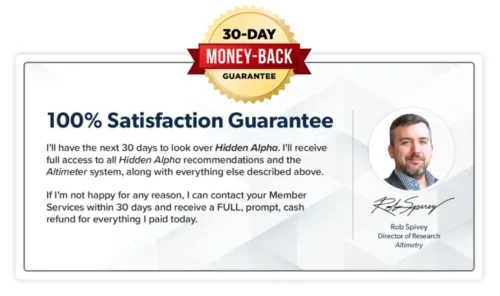

Every subscription to Hidden Alpha is covered by a 30‑day, 100% money‑back guarantee.

That means you have a full month to explore the research, test the Altimeter database, and review the bonus reports with no risk.

That means you have a full month to explore the research, test the Altimeter database, and review the bonus reports with no risk.

If you decide the service isn’t for you, a simple call or email to the customer service team will get you a prompt refund, and you can still keep all the reports you’ve received.

However, similar services in this newsletter’s price range also offer 30-day refunds. So I usually wouldn’t give extra brownie points for following the norm.

That said, I do appreciate that Hidden Alpha offers unrestricted access to the Altimeter System during the satisfaction guarantee period.

Hidden Alpha vs Other Stock Newsletters

If Hidden Alpha’s setup doesn’t resonate with you, consider one of these other platforms I’ve reviewed. Note that each of these are unique services and aren’t affiliated with one another.

Hidden Alpha vs Motley Fool

I find Hidden Alpha and Motley Fool to run in some of the same lanes, trying to unearth stock picks with potential before all that growth happens. How they go about it is a big different, but both have a team of analysts looking through all the noise for these opportunities.

Motley Fool’s Stock Advisor is probably the closest comparison, and it does tend to offer a few more stock picks than Hidden Alpha each month. The research you receive is a bit more surface-level though, and there’s no Altimeter to do your own research with.

Hidden Alpha vs Similar Alpha-Focused Services

Hidden Alpha has carved out a unique niche among services targeting alpha stocks thanks to its forensic accounting (their words, not mine) approach to finding mispriced or undervalued stocks.

I will say that the picks I see here rarely fall into portfolios from other platforms, for better or for worse.

Morningstar and Zacks have large databases and a huge reach, but don’t match Hidden Alpha’s depth of research into its findings. If you want a wide range of opportunities, you may want to look elsewhere. If you want conviction behind recommendations, stay right here.

It’s a unique tool for vetting stocks that tacks on a lot of value to the overall package.

Tags:

Tags: